Việt Nam stocks trade at crisis-level valuations despite robust business outlook: VinaCapital report

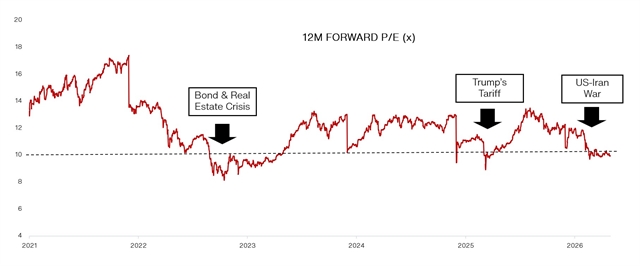

Despite expectations of 15 per cent earnings growth in 2026, the VN-Index is currently trading at just 13 times forward price-to-earnings (P/E).

HCM CITY — Despite expectations of 15 per cent earnings growth in 2026, the VN-Index is currently trading at just 13 times forward price-to-earnings (P/E).

Even more strikingly, more than 70 per cent of listed stocks are valued at less than 10 P/E, a valuation consistent with past crisis conditions, according to VinaCapital Fund Management JSC.

In a report, Michael Kokalari, chief economist at VinaCapital, said this apparent disconnect is largely driven by the exceptional share-price performance of companies within the Vingroup ecosystem, whose firms now account for nearly 30 per cent of the VN-Index's market capitalisation.

A significant portion of other stocks was being valued at levels typically associated with an economy in crisis, despite Việt Nam's resilient growth, booming high-tech exports and the strong fundamentals of many listed companies.

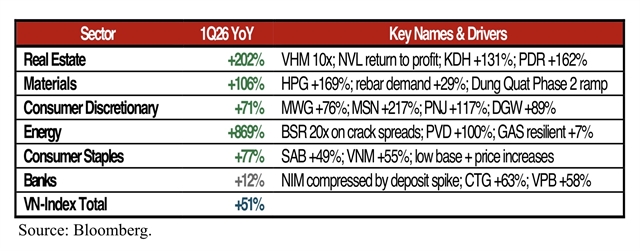

Aggregate earnings for VN-Index constituents had surged 51 per cent year-on-year in the first quarter, substantially outperforming the market consensus forecast of 15 per cent growth.

While the sharp increase in earnings by Vinhomes (VHM) had contributed to the overall result, earnings had still expanded by around 30 per cent even after excluding VHM – double the consensus estimate.

The growth had been broad-based, supported by strong performance across the real estate, materials, retail, energy, and consumer staples sectors.

Việt Nam was advancing a wide-ranging series of reforms aimed at improving the efficiency of state-owned enterprises, supporting its inclusion in the FTSE Emerging Markets Index, and accelerating the restart of stalled real estate projects, among other objectives.

“We do not think the full impact of these reforms has been priced into the stock market yet since the benefits will accrue gradually through better liquidity, more listings, SOE restructuring and the reactivation of delayed projects.”

With a small number of large-cap stocks significantly influencing the earnings performance of entire sectors, active portfolio management and careful stock selection remained critical for investors seeking to maximise returns.

The market faced several challenges, including prolonged disruption in the Strait of Hormuz, a widening trade deficit, rising inflationary pressures, higher interest rates and persistent foreign capital outflows.

Foreign investors had sold US$2 billion worth of Vietnamese equities this year, following net outflows of $5 billion in 2025.

Nevertheless, the Government possessed sufficient policy tools to mitigate these risks.

Việt Nam’s high-tech exports had risen 49 per cent year-on-year in the first four months of this year, following a 48 per cent increase in 2025, driven by strong global demand for AI-related products.

Yet, the country’s trade deficit had widened from around 3 per cent of GDP before the conflict to more than 6 per cent by mid-May, equivalent to around $13 billion.

But much of it had stemmed from rising imports of intermediate and capital goods needed to support the rapid expansion of the high-tech manufacturing sector.

Foreign-owned high-tech companies were increasingly importing capital goods used in the production of precision components, an important but nuanced point that helped explain why the currency and stock markets were brushing off the recent jump in the trade deficit.

Imports of components like chips and specialty glass typically used in the production of smartphones were consumed within three to four months of being imported.

The payback period for capital equipment used to produce export goods was considerably longer than the typical three-to-four-month turnaround cycle for components used in high-tech manufacturing, causing a “J-Curve” effect in which the trade balance first declined and then improved as imported capital goods and components got used to make exports. — BIZHUB