JLL: Việt Nam data centres poised for growth

Việt Nam’s data centre market is on a growth trajectory, offering ample opportunities for expansion, experts said.

HCM CITY — Việt Nam’s data centre market is on a growth trajectory, offering ample opportunities for expansion, experts said.

The country’s data centre market is developing alongside rising data processing needs, the spread of artificial intelligence and enterprise digital transformation.

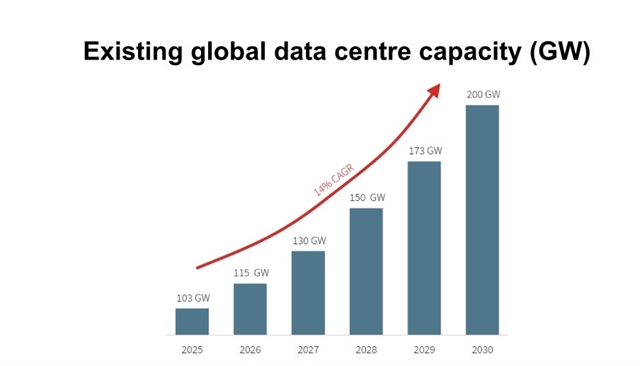

Research from JLL indicates global installed capacity could increase from roughly 103 GW to 200 GW by 2030, supporting an estimated US$3 trillion of infrastructure investment over the next five years.

They added that Hà Nội and HCM City have a combined operational capacity of around 60 MW. While this is currently lower than regional hubs such as Jakarta, Kuala Lumpur, Bangkok, and Manila (74 MW), it demonstrates strong potential for future scaling.

Currently, the majority of supply is provided by key operators, including VNPT, Viettel IDC, FPT Telecom, CMC Telecom, HTC (ECODC), and QTSC, all of whom maintain data centres to Tier III/Tier III+ standards. This ensures readiness, security, and service continuity, laying a solid foundation for the market’s future growth as businesses increasingly seek reliable, outsourced infrastructure and cloud solutions.

Across Southeast Asia, capacity is scaling quickly. Between 2023 and 2028, indicative growth trajectories show compound annual growth rates ranging from the low‑20s to high‑30s percent depending on the market.

Việt Nam is expected to follow a similar path, lifting total capacity and diversifying services as enabling conditions improve. The market has already seen a number of new developments announced or underway, including Viettel IDC’s data centre in HCM City with a designed capacity of up to 140 MW. Kinh Bắc City has also partnered with AIC and VietinBank to develop a nearly $2 billion data centre in Tân Phú Trung Industrial Park, targeting up to 200 MW of IT Load. Meanwhile, the CMC Hyperscale Data Centre is being developed with an investment of more than USD250 million, offering an initial capacity of 30 MW and expandable to 120 MW.

Trang Lê, country head of JLL Vietnam, said: “Artificial intelligence has become infrastructure. Power, data and execution speed will separate leaders, and Viet Nam has the momentum to join them.”

Demand fundamentals are supported by a young, digitally engaged population, high smartphone usage and heavy data consumption across social media, on‑demand video, e‑commerce and online gaming. Enterprises in finance, technology and services are accelerating digitisation, increasing needs for big‑data processing, internet‑of‑things connectivity and a move from on‑premise systems to outsourced models.

On the supply side, Việt Nam offers competitive commercial electricity pricing in the regional context and a meaningful share of renewable energy from hydropower, wind and solar.

Power Development Plan VIII was approved in May 2023, with an implementation roadmap released in April 2024, targeting around 155 GW of national generation capacity, diversifying away from coal and progressing toward direct power purchase agreements for large users. International connectivity is improving through subsea cable landings and plans for two to four additional systems in the next five years.

In land markets, industrial and high‑tech parks near major cities are preferred; data centre‑ready sites often carry a 30–50 per cent premium over standard industrial plots due to infill locations, dedicated substation requirements and fibre readiness.

The regulatory framework is moving in a favourable direction, JLL said.

The Telecommunications Law 2023 took effect on July 1, 2024, with provisions on data centre and cloud services effective from January 1, 2025, allowing 100 per cent foreign ownership in data centre services under a lighter‑touch regime than traditional telecom. The Land Law 2024 (effective January 1, 2025) clarifies land categorisation for postal‑telecom‑IT works and allows foreign‑invested enterprises to acquire land‑use rights transfers within industrial parks and high‑tech zones under specified conditions.

Execution risks include power availability, transmission capacity, grid‑connection timelines, supply chains, and talent. Northern Viet Nam has experienced periodic power tightness in recent dry seasons, underscoring the importance of transmission upgrades and diversified generation. Globally, grid‑connection queues exceeding four years and equipment lead times of about 33 weeks have prompted interim solutions such as battery energy storage and, in some markets, on‑site power. Viet Nam will also need to scale a workforce trained to international standards in design, construction, and operations through targeted programmes and industry–university partnerships.

The outlook to 2030 is constructive but contingent on progress across power, land, subsea capacity, procedures, and talent. Commercially, high‑density AI workloads are poised to lead pricing dynamics, while retail co-location remains a bridge for enterprises transitioning from on‑premise to cloud, the company said. — VNS